Contents

Meaning of Business Income

Usually, income earned by an individual is classified into 5 heads as per income tax. They are

- Income from salary

- Income from house property

- Income from profits or gains of business or profession

- Income from capital gains

- Income from other sources

These are the main heads under which incomes are classified. All incomes earned by the person under the act will be classified into the following. In this article, we will look deep into the income earned from the business.

Understanding Business Income

Any income earned from a business or profession is called business income. As per the Income Tax Act, the business includes any venture to make profits and profession means any activity rendered by an individual with his specialized knowledge or his intellectual skill.

It may be the price of the product delivered or the fees for the service rendered by him or her. This income is chargeable under Section 28 of the Income Tax Act. Business income includes capital gains from business, fees for service rendered, the monetary value of the perquisites enjoyed by the taxpayer, compensation received by him against any property in the name of the entity, income from different speculative transactions etc.

The main item that constitutes mostly in business income is the income or revenue earned from the sales of the entity. The tax rate for any domestic company whose total turnover does not exceed 400crores for the PY 2021-22 will be 25% and any other company will have a tax rate of 30%.

Business income can either be profit or loss. It depends on how much the firm has earned and the expenses incurred by the firm in the year.

Let us now see how the business income is calculated.

Calculation of Business Income

As we said earlier setting off the expenses with the income earned is how the business income of the entity is calculated. There are certain deductions also available to the entity while calculating the business income.

The income earned from the business is:

Profit/Loss from business = Income earned from business- Expenses incurred in business

If income is more than expense it will result in profit. Likewise, if expenses are more than the income it will result in a loss. Either way, the business is entitled to calculate the income earned from the business.

After calculating the raw income earned from the business there are certain deductions which are exclusively applicable in the calculation of the income earned from the business. These are deducted from the gross total income. After the deductions, the amount which stands against the account is the amount which is taxable under the head as business income.

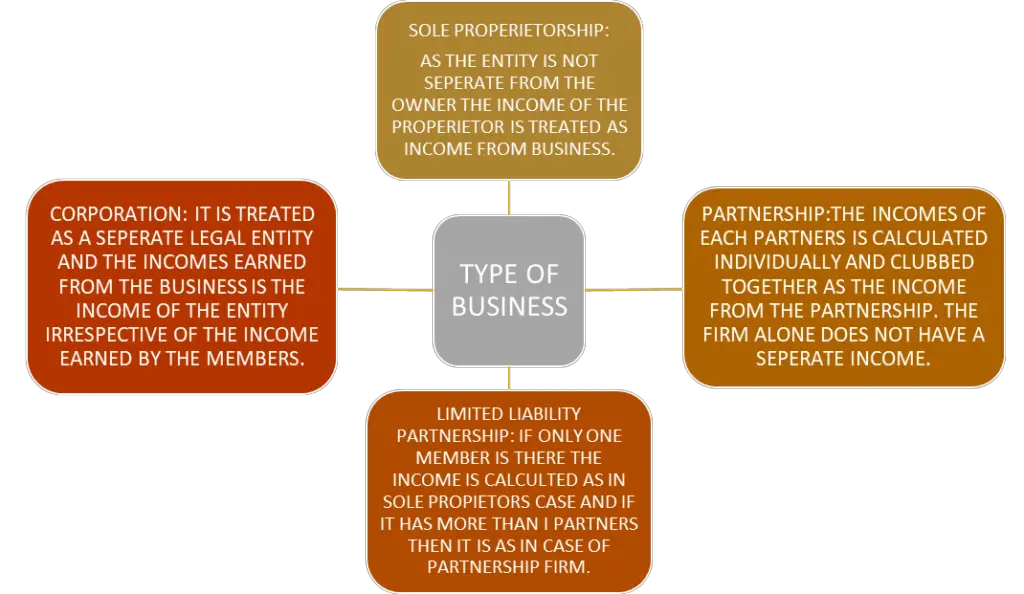

Based on the type of business they carry out their taxable amount differs. As we know there are mainly 3 types of business: sole proprietorship, partnership and corporation.

As we can see even though the income earned is the same it is treated differently according to the type of business carried out by each firm. Basically, we can say:

Business income = (Income – expenses) – deductions

I.e., Taxable business Income = Gross total income – deductions

Now we have understood what is business income. Let us now see the different examples of business income raised from business as well as profession.

Examples of Business Income

To understand this concept in a clear way let us divide the incomes as income earned from business and income earned from profession

| Income from Business | Income from profession |

| Sale of a product | Fees for the service rendered under the profession |

| Salaries in the case of a partnership firm and income of the owner in the case of a sole proprietor | Sum received against copyright or intellectual property right |

In real-life instances:

An advocate has practised on his own in the high court. The fees he collects from his clients are treated as income from the business. In the same case if the advocate is a partner of a partnership firm his fees is treated as the income from the business of the partnership firm.

Let us look into another example of speculation income:

When the income from speculation traded as stock is treated as income from business or else it is treated as income from other sources.

In short, different incomes arise and these incomes are classified into the heads like the source in which they arise, to whom it arises, and how it arises. Usually, business income arises on the course of action of the business and is a continuous process till the termination of the business or the profession.

Conclusion

Business income is every income that arises to a taxable person under the law through either business or profession. They are liable to pay tax under the Income Tax act irrespective of the type of business which is carried out by the person. In short, we can say that whether the income is positive or negative i.e., it is profit or loss the business is accountable to record this under the act. Setting off the expenses against the income will give you the gross amount of business income and when we deduct the deductions under the act, we get the taxable business income.