Contents

Meaning of Fixed Deposit

Fixed deposit is the method of doing investments in India. In this, some amount of money is deposited for a fixed time span which is decided by the individual who is depositing his funds. The time span of the fixed deposit could be from 7 days to 10 years. This financial provision is generally offered by banks and NBFCs. After depositing the money, a fixed rate of interest is added and given to the individual. The rule followed for the fixed deposit is that one can withdraw the money even before its maturity, but if he does so, he needs to pay a fine for the same.

Advantages of Fixed Deposits

Assured rate

The biggest reason for people prefer fixed deposits for their funds is that they provide a fixed and assured rate of return to the individual, i.e., it is guaranteed that you will receive the mentioned rate of return, once you invest the money in the fixed deposit account. Different banks have different rates of interest on amounts that they publish on their website so that it is easy for the individual to know the amount of money he would be getting after a particular time span.

Tax threshold

Banks do not deduct tax on the interest until the amount of 10,000 is crossed, which means that unless an interest of 10,000 is earned by the individual in total from different fixed deposits, the bank won’t charge and deduct tax from the individual. Thus, it proves to be comforting for small deposit holders.

Flexible tenure

The time span for which the person wants to continue the fixed deposit is flexible and is totally dependent on the person who is investing his money. Once the fixed deposit is mature, the individual has the right to decide whether he wants to extend and continue his fixed deposit for the same time span or not.

Easy to discontinue

It is easy to destroy a fixed deposit. Fixed deposits that are booked online can be destroyed online too through net banking, and even banks have different ways to destroy the fixed deposit if the individual wants.

Loans against a fixed deposit

A fixed deposit is something on which a person can depend at the time of need. Applying for and taking a loan against a fixed deposit is not difficult. One can take out a loan for about 95% of the amount of the fixed deposit. It varies from bank to bank.

Safe investment

Savings, which are done in form of stocks and mutual funds, depend on the market and fluctuate with time according to the market, i.e., if the market goes down and is at a loss, so is the person’s money. But the fixed deposit is a safe form of investment. The money that the person will get after a span of time is fixed, which makes it a safe investment option.

Multiple fixed deposit accounts

A person can have many fixed deposit accounts at the same time. One can open a new fixed deposit account whenever a person wants to make an investment, no matter how many accounts he is having currently, he can always open a new one.

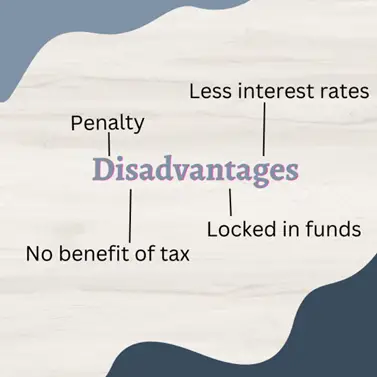

Disadvantages of Fixed Deposit

Reducing interest rates – The disadvantage of fixed deposit is that as the prices in the market increase, the interest rate still remains the same. It does not change. With time, the interest rates have been reduced in the case of fixed deposits, and as a result, people do not prefer to invest their funds in fixed deposits.

Locked in funds – The money you deposit in a fixed deposit gets locked up and is not available unless the funds are prematurely withdrawn.

Penalty – An individual who deposits their money in a fixed deposit is charged for penalty if they wish to withdraw their money prematurely, which is mostly less rate of interest given to them.

No benefit of tax – The benefit the individual earns from the interest of fixed deposit is negligible as it is added to the individual’s taxable income.

Fixed interest rate – The rate of interest which was at the start of the fixed deposit remains the same until the deposit matures; even though the rates have increased, the bank still gives the same interest rate to the individual.

Uses of Fixed Deposit

1. It helps the individual to earn more as it has a high rate of interest than any savings method.

2. The funds of the individual remain secure in a fixed deposit. It is a one-time effort in which an individual needs to deposit a good amount of money that can be invested, which would keep increasing depending on the interest rate.

3. It gives you returns for sure once you invest your money in it no matter how badly the market fluctuates.

4. It is a way that lets the individual grow his savings with low – risk.

Conclusion

Fixed deposits are a way for people to gain benefits with less risk appetite. Through saving, a person gains fewer benefits but would be fixed. The fluctuation in the market will not affect it. The individual here will not experience any loss of his money. The person can also discontinue his fixed deposit at any moment he wants by prematurely withdrawing it. It can benefit a person in the long run in which the person has deposited a lump sum amount of money in fixed deposit and can wait for a time period of his choice of about 7 days to several years and see his money growing depending on the interest rate of that particular bank in which he has invested his money.

By considering its advantages and disadvantages, it is considered to be a great method for people to save their money who do not want any kind of risk with it as in other methods the interest rate depends on the outside market too, and if the market falls the individual will experience loss. So it is a method of investing your money and gaining some benefit with very less risk.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.bh/register?ref=IXBIAFVY

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://accounts.binance.com/si-LK/register?ref=LBF8F65G