In a company, there are always two parties. One is the employer who offers the job, and the other is the job seeker employee. The main motive of an employer is to attract a pool of potential candidates for a particular job and to retain them. On the other hand, the main motive of an employee is to earn more and more while delivering their services to the company.

However, at times, it becomes difficult for an employer to retain an employee. This is because the employee leaves the company if they are paid well enough at another company. To avoid this type of situation, the employer offers various other benefits to the employee. Such a benefit is the employee stock option plan.

Contents

What is an employee stock option plan?

Employee stock option plans, or ESOPs, are benefits given by a company to its employees. In this, the company issues its equity shares to its employees at a discounted price with a view to encouraging them to work for the company. All companies except listed companies can give ESOPs by the Companies Act of 2013 and the Companies (Share Capital and Debenture) Rule 2014. In the case of a listed company, the ESOPs are issued following the rules and guidelines provided by the SEBI.

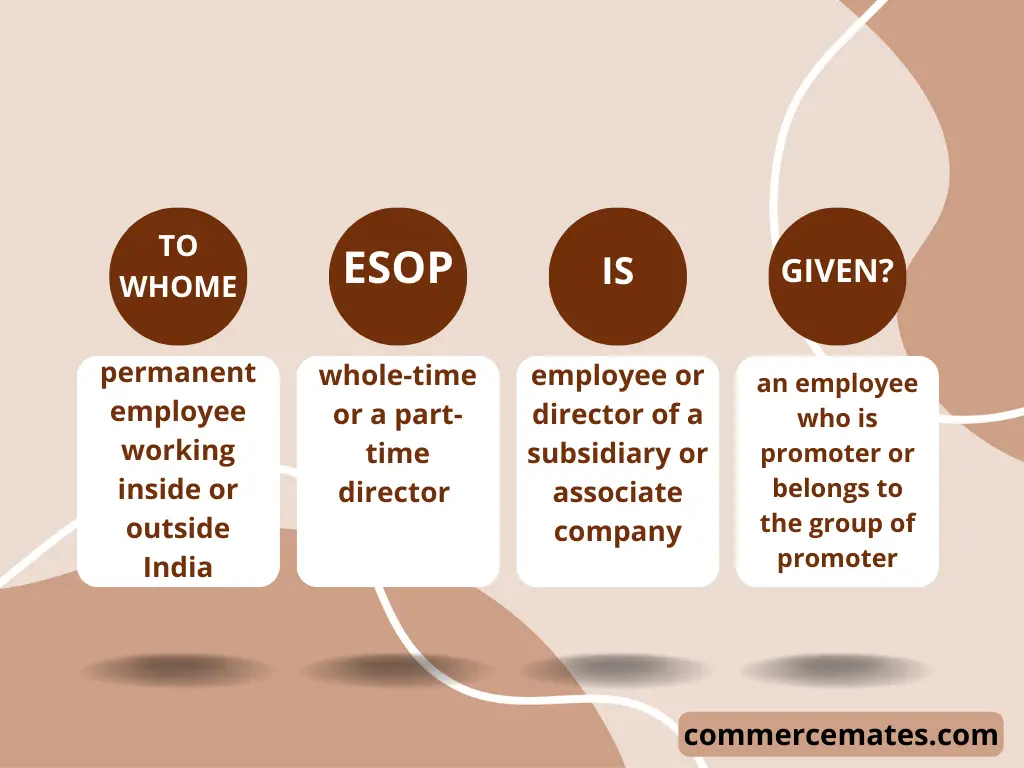

To whom the benefits of ESOP are provided?

ESOP can be issued in some cases only. According to rule 12(1) of the Companies (Share Capital and Debenture) Rule, 2014, the following are the cases where it is given:

- An employee who is permanent and working in India or outside the boundaries of India.

- A whole time or part-time director but not an independent director.

- A permanent employee or whole-time director or part-time director of a subsidiary or an associate company in India or outside the territory of India.

- An employee who is either a promoter or belongs to a group of promoters.

The Process of Issuing ESOP

The provisions relating to the issue of ESOP are given under section 62(1)(b) of the companies act 2013 and rule 12 of the companies (share capital and debenture) rule 2014. According to these rules and guidelines provided in these rules, the process to issue ESOP is as follows:

- A draft of ESOP is prepared by the company in compliance with the Companies Act 2013 and Companies Rule 2014.

- Notice is given to the board of directors regarding a meeting to pass a resolution of the ESOP draft.

- The notice is provided at least seven days before the meeting to all the directors.

- Resolution is moved in the meeting to determine the price of shares, persons to whom it will be issued, timing, and date.

- A copy of the draft is sent to all the boards of directors within 15 days of its conclusion.

- A copy of the MGT-14 form given by the registrar of the company is also passed to the boards of directors along with the draft of ESOP.

- A meeting notice is sent to the directors, auditors, shareholders, and secretarial auditors of the company. This notice is given at least 21 days before the meeting.

- A special resolution is passed for the issue of ESOP to the employees, directors, and other designated members of the company.

- After passing the special resolution, an MGT-14 form is filed with the registrar of the company. This form has to be submitted within thirty days of passing the resolution.

- The option is sent to employees, directors, and other designated members of the company.

- A “register of employee stock options” is maintained in form no SH-6 containing the details of the employee, director, and other persons to whom ESOP is granted.

Note

In the case of a private company, the company can issue ESOP only if it is allowed or permitted in its Article of Association.

If it is not permitted in the AoA, then the company first call for a general meeting to alter the specific provision in its AoA and then hold a board meeting for passing and approval of the ESOP resolution.

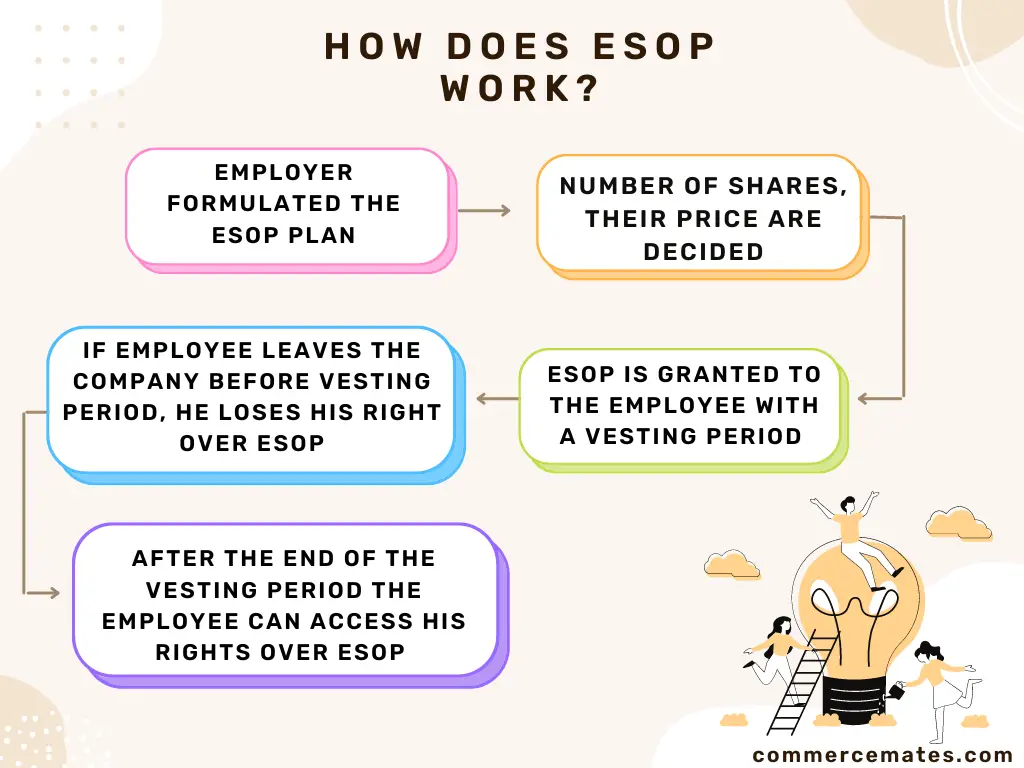

How Do Stock Options Work for Employees?

ESOP works in the following ways:

- An employer decides the number of shares to be issued under ESOP, their price, and to whom they will be issued.

- ESOP is then granted to the employee with a specified date of grant.

- After ESOP is offered to the employee, a specified period is set which is called the vesting period.

- According to the vesting period, the employee can avail of the benefit of stock ownership only if they stayed in the company for the given period.

- If the employee leaves the company before the given period, they will be unable to avail of the benefit under ESOP.

- Once the vesting period is ended, the employee gets all the rights over the ESOPs.